Would you like to start a conversation with other industry leaders to brainstorm a challenge or to just know more on a particular topic?

Engage in online discussions with your Peers

Start Now

Romi is the recipient of the “BPM Achiever in Global India” award from the Shared Services Forum (SSF) India. This is an article based on his presentation at the SSF’s 9th Annual Global Business Services Conclave on December 13, 2019 at Bengaluru.

–ed

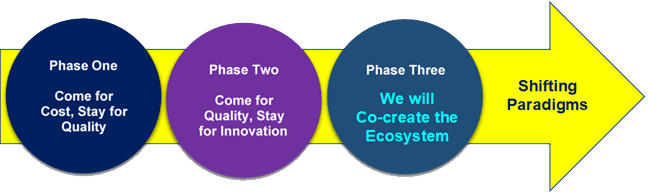

I have had the privilege over the past three decades to be a part of the evolution journey of the Business Services industry. Let me share with you a peek into the genesis of the industry as I saw it. For the sake of simplicity, I will try and surmise the journey into 3 phases which reflect the past, present, and future of this phenomenon which morphed into an industry.

Phase 1: Come for Cost, Stay for Quality (approx mid 1990s to 2007)

Phase 2: Come for Quality, Stay for Innovation (approx. 2007 to now)

Phase 3: The future – The new CoE (Core Operating Environment)

For the last few decades, there have been disruptions all around us – the rise of high-speed internet, a rapid change in computing speed and processing power, an ever-decreasing costs of storage, and democratisation of data and technology. All of them have dramatically changed how we live, interact, and how businesses operate. These disruptions have caused organisations to question status quo and push boundaries to outperform. Almost centre stage to these disruptions has been global sourcing of work – which started as a cost arbitrage and grew into something significant with far reaching implications and exponential growth for the industry in India.

It was an illustrious journey, not just because it created millions of jobs, but firmly established brand India globally. However, there never was a grand plan to carve out an industry as we see today. The story started experimentally, with a handful of inventive leaders in the mid-90s. Then it grew from strength to strength.

Let us step back to see a panoramic view of this evolution.

Phase 1: Come for Cost - Stay for Quality

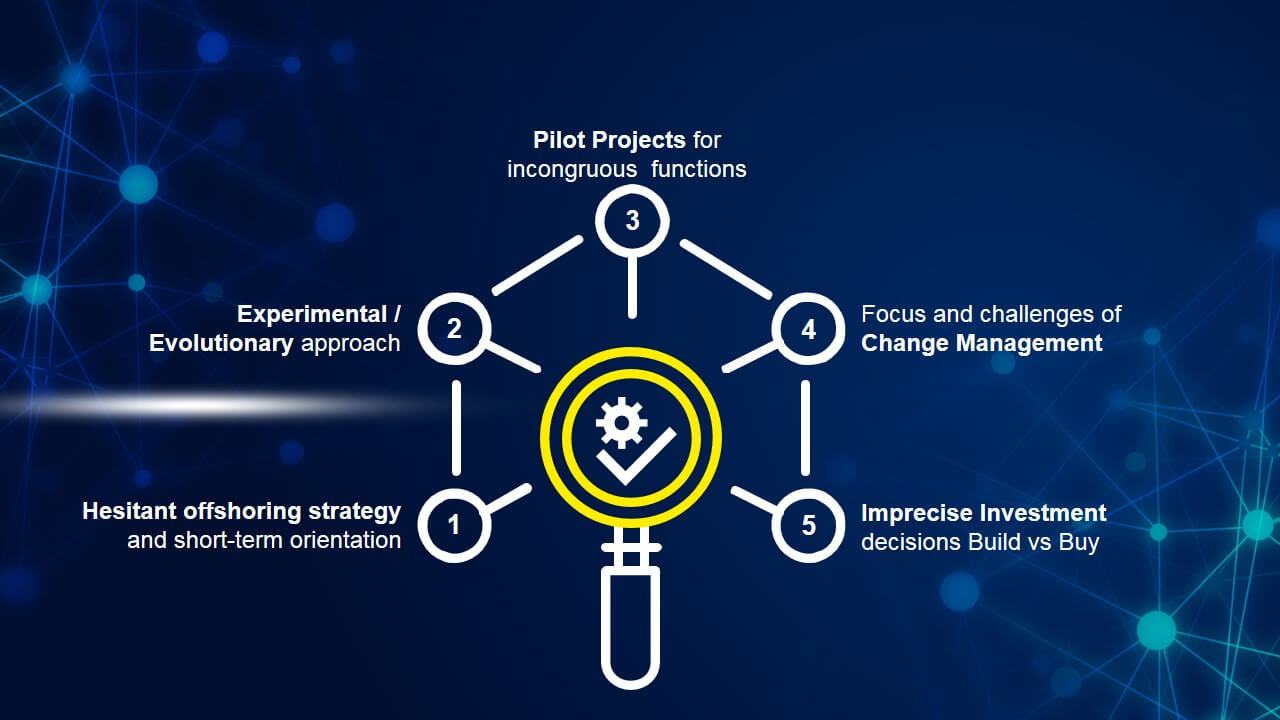

This was the embryonic stage of the industry when we were trying to define new models of outsourcing to large global companies. The approach was a cautious ‘toe in the water’. It was experimental and without any grand strategies in most cases. I was then in GECIS (now Genpact) and we were trying to sell the concept internally to the myriad group companies to start with. “Come for cost, stay for quality” became our tagline. There was scepticism, hesitancy borne of uncertainty and a propensity to look at low risk areas.

This worked fine for operations like ours, since we were finding our path and building our product maps. Trust was built surely but slowly. Often there were disjointed pilots and they were driven by brave champions of the sending centres.

Another manifestation of this indetermination came to the fore as captive centres started mushrooming in India. However, there seemed to be an arm's length distance from the mothership or the parent company. So much so, they even called them by another name. Standard Chartered’s service centre was called SCOPE; Bank of America’s was called Continuum, and so on. Even the third-party providers seemed unsure. For instance, Infosys BPO was called Progeon; Satyam called theirs Nipuna; Wipro acquired a BPO and did not call it Wipro - they continued to call it Spectramind. It was probably a risk mitigation strategy to protect the mother brand in case the experiment did not work.

Many of the most successful Global Captive Centers were created by

leaders who came from outside the organization.

This was true even when the organizations had been in the country for a

very long time, had a very large workforce in India and had some great leaders to boot.

Then there were the learnings around change management. Many companies underestimated the effort and pain of change management that were required. As pioneers in the field we created some toolkits for transitioning work smoothly. I daresay many of those toolkits are still alive in many organisations, decades later. A trend that I noticed much later defined as another success factor in the journey. Many of the most successful Global Captive Centres were created by leaders who came from outside the organisation. This was true even when the organisations had been in the country for a very long time, had a very large workforce in India and also had some great leaders to boot. Whether it was GE or Standard Chartered or BankAm, there seemed to be a strong preference to get leaders from outside, to set up their GCCs. It probably had to do with getting an individual who had no baggage within the organisation, who could be objective, entrepreneurial and disruptive enough to make it happen.

Another element that kept the conversation alive was the quintessential build-or-buy decision. There was no right or wrong, or black and white. Depending upon how much you tortured the spreadsheet, it would confess to what you wanted. There were companies, which spent a lot more than what they would save in two years, on something as simple as site analysis for choosing the location for the GCC. Yet other companies engaged global consultants to help them decide or find third party service providers. Soon, even companies that had no business presence in India began to favourably look towards us for servicing.

According to a McKinsey study in 1997/98, the BPO industry was predicted to reach US$8 billion in the next 8-9 years. This prediction was never taken seriously because the industry was not even US$100 million. But successes multiplied. Fast forward to today, we are a US$25 billion industry. It will be fair to say that the IT services industry was also maturing around the time. While the “Made in India” label was never respected, the “Serviced from India” label began to find feet firmly.

Of course, there were challenges along the way. There was no ready talent pool – it had to be created. We hired from every conceivable industry. Telecoms costs were astronomical, compared to today. Support functions were getting used to the services industry. We were all trying to understand the cultural nuances and global quality expectations. Geography was becoming history. It was a hyper growth phase and terribly exciting.

Phase 2: Come for Quality - Stay for Innovation

This was the second phase, built on the strong foundation of the first phase. It came with different challenges. We are probably at the last leg of this phase today.

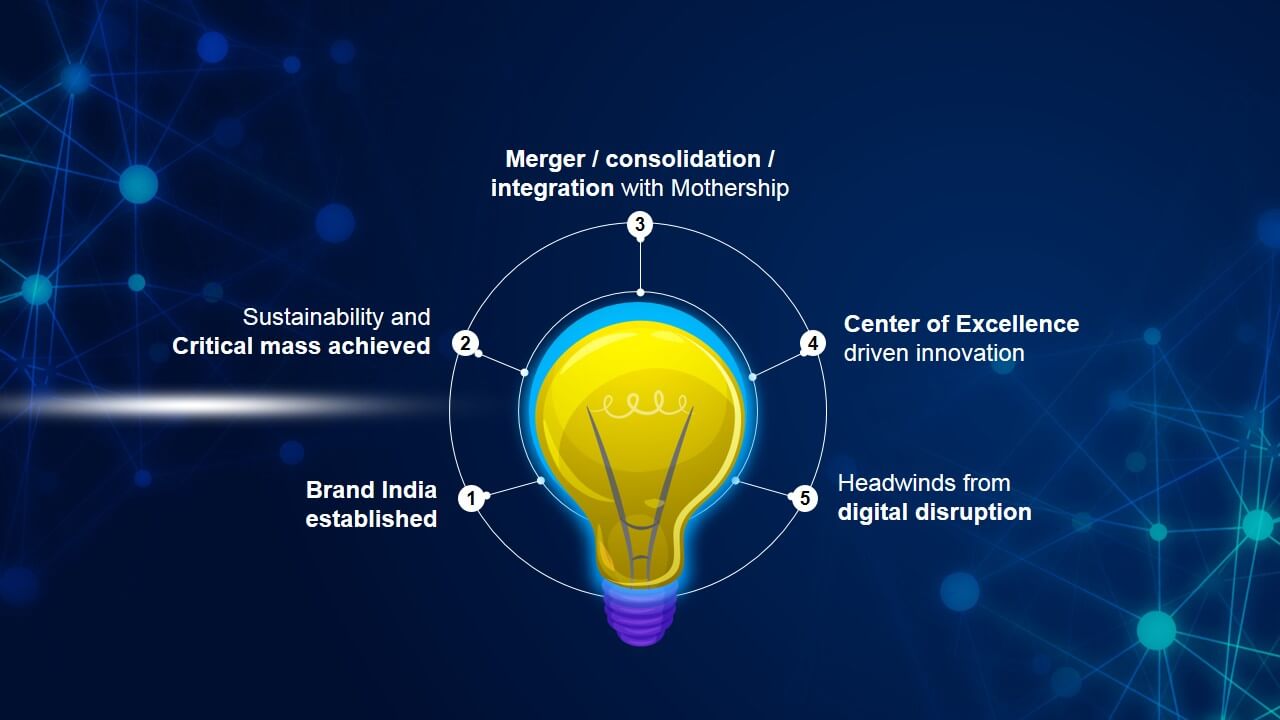

If we look at the last decade or more, brand India is clearly established. Cost savings was almost a given and organisations created and scaled up their shared services centres. The slogan changed to “come for quality, stay for innovation.” High expectations replaced scepticism. From an option, India became the obvious, if not the necessary destination. Organisations are now willing to bet big dollars on creating and delivering services from India. Millions of square feet of commercial real estate has come up in the last few years to cater to this growing demand.

As the GCCs matured and garnered deeper understanding of the migrated processes, innovation became the obvious next step.

Many companies today create products and services that are conceptualized, designed and created in India - and then deployed globally. The journey from data entry and call centres to RPA and Analytics is real. The lines between delivery and innovation centres is blurring. This is possible because of the critical mass, deep domain understanding and the high quality of talent driving these innovations. Regardless of the market share for their products in India, the largest talent base of most global organisations outside of their home countries is right here in India. Innovation has become mainstay in GCCs today. From process training to design thinking and from process mapping to creating products, the journey has been transformational.

Innovation has become mainstay in GCCs today.

From process training to design thinking and from process mapping to

creating products, the journey has been transformational.

This is also the time when the GCCs gained acceptance and respectability within the larger organization. Integration with the mothership happened. For instance, SCOPE became Standard Chartered India, Progeon became Infosys BPO etc. And in many cases, the distance between the India leaders and the global CEO became shorter. The value of the GCCs was not just within the organisation. PE and VC firms put huge valuations and GCCs became tradable assets with significant worth.

As we enter the next decade, existing paradigms are all set to be challenged again. The new set of challenges now threatens the very existence of models, which made the industry what it is. While the labour arbitrage and innovation mindset still have their value, the application of the same is undergoing a radical and resolute transformation. RPA, self service, IOT, Analytics and AI threatens to eradicate a number of processes that run in the current service operations. How we cope with these challenges will determine our success in the next phase.

Phase 3: Co-creating the Ecosystem – The Hereafter

The new definition of a COE is not “Centre of Excellence” it is “Core Operating Ecosystem”. If you look at the most successful business models across the globe, they are all about creating a whole new ecosystem, often based on a strong technology backbone. Some obvious examples are Uber, Amazon, Alibaba, Visa, etc. Process and skills will still be important at the micro level of work; but the competitive advantage to be gained by re-aligning the business model will be the imperative. The question will become the ability of our centres to create or help in the major transformations that need to be done.

The future in phase three is going to start by understanding what ecosystem we are part of - not only playing in it, but also creating it. And if this sounds a little abstract, it is because we don't know what is sitting out there to disrupt our businesses. Large businesses have been disrupted overnight, more so now than in the past, and this will continue to happen. Understanding how to integrate technology with physical resources to create value for the clients and the business will be key to success.

Sources of competitive advantage are changing. There was a time when data gave us the competitive advantage.

Today we have more data than we need.

The advantage lies in the analytics and its deployment to make

real-time decisions. Today, data also decays fast; it has a finite

life, especially as edge computing gains currency.

Similarly, there have been other subtle but definite changes in the sources from where companies get competitive advantage. For instance, knowledge and skills are more obtainable, culture and talent are not. Corporate structure can be easily copied, corporate flexibility and innovation is tough to replicate.

In the past FTEs was a measure of success - that's what we grew up with. Having more people meant we were bigger and stronger. That's going to change. How value is added is going to be more important on the measuring scale. We are aware of how AI or ML or RPA is impacting the workforce. We are already experiencing it and the pace will only accelerate. The talent mix in the GCCs will necessarily need analytics and data science skills with an understanding of what AI can do. Then sponsors at the horizontal or vertical business lines will need to empower these teams to transform.

‘Agile’ is clearly the new norm.

Corporates and economists have stopped looking at

five-year horizons.

Even one year seems too long to plan for. Things like five-year plans, three-year outlook are out-dated and will not work in the current scenario. Agility will come down to a daily chore, for what we do and for everything that we do.

Another big change going forward is that ‘machines’ will become the biggest customers for some of the businesses. For example, soon our refrigerator may start ordering our groceries. AI algorithms will decide what is required, indent it, place the orders, monitor delivery, pay for it and be done with. Machines will order other machines and machines will take care of customer service. Even if autonomous cars start whizzing around, accidents may still happen. Determining which machine was at fault will be the job of another AI algorithm.

Now, as an industry, we need to peek into the future and determine our role/s in shaping and running it. The emphasis has to shift very quickly from being focussed on our customers to understanding what is the emerging ecosystem for our customer’s customer.

The ecosystems that we create today, will determine the

future of the business. The Core Operating Ecosystem that we create will

drive our strategies, success and operating models.

Let us take a live example of co-creating the ecosystem.

A well known service company does claims processing for one of the largest insurance companies in the world – at an average cost of X dollars in an average period of two weeks per claim. A goal was set to reduce claim processing cost and time. Conventional methods would set a target and be happy reducing both time and cost by say 10-20%. But the big question was if 20% was the right number. Why not 10 or 80? Was that even achievable?

In a classic case of co-creation, the insurance company jointly with the servicing unit built an ultra-efficient and cost-effective way of doing the process. For instance, if there is a storm-caused damage to one of the customers’ house, the traditional process demanded a lot of paperwork. Surveys had to be carried out, estimates had to be drawn, the claim would have to be authenticated, adjudicated and then paid. The whole process could effectively run into a few weeks. Today, per the revised process, the insured person files a claim on an app, taking photographs of the damage and uploading them. An AI engine takes a look at these photographs, verifies if there was a storm, fetches the data from the met department, sends out a drone to capture images, looks at the images that come back, decides on the veracity and validity of the claim, looks at the amount, and pulls an estimate for the repair and throws up a decision. All of this, which normally would have taken a long time for an individual is being done through an AI/ ML interface that has been co-created. It then estimates the probability of the claim being false or a fraud. Further it also suggests if the amount should be paid off without any further analysis, especially if the fraud percentage as well as claim amounts are low. It might just cost the company more to investigate the claim than its value and risk it warrants.

So, the whole process, which normally would have taken 2 weeks is completed in less than a few hours, and that if there is a drone that goes and comes back, otherwise it would take only a few seconds! The customer is happy, the errors are reduced, time is crunched and a new ecosystem is at work leveraging data and technology.

Had the company set the bar for a cost cut of 20%, they would have been way off the mark.

The cost came down by 80% and processing time by 90%.

This is what we call disruptive.

Every business is facing some or the other form of disruption today.

This leaves us with the quandary as a leader – we can continue

to squeeze the towel and be happy with incremental gains, or we can be

co-creators of new ecosystems driving transformational change.

The Future of the Industry and the Wheel on Bag Challenge

The wheel was invented in the Stone Age, a few thousand years ago. People have been travelling around even before that. Since the very beginning people have been carrying all sorts of bags, suitcases or trunks while travelling. Both, the wheel and the bag have been there forever. But it was only in 1972 that someone put these two together to create a strolley or the rolling bag. That changed the life of the baggage companies forever and the way we travel. Today, we cannot buy a suitcase without wheels. Strangely, it took thousands of years for two obvious things to come together.

In every field of work being done across organizations and industries, there is a ‘bag’ and a ‘wheel’ sitting there. From a disruption and an innovation perspective, it is impossible to believe that nothing can be done, though we might not see it today. Someone will put the two together and it will then seem so simple and obvious. The challenge is to co-create and put that wheel on the bag. and to predict and create the new ecosystem. That is how evolved companies are behaving – and that’s how India and her leaders can set themselves ready to rule the future.

ABOUT THE AUTHOR

With over 35 years of leadership experience in industries ranging from Manufacturing, Information Technology, Banking, Consulting, Outsourcing and Leadership Development, he is a seasoned general manager. As a pioneer in the outsourcing industry in India, since 1996, he has contributed significantly as part of the initial leadership team that set up Genpact. He also set up the KPO business for GE Capital; set up Scope International (the global centre for Standard Chartered Bank) with a number of pioneering initiatives; and grew the Dell India centres to make it one of the largest GCS in the country. He has been the Managing Director for DXC Technology in India, and is also on the board of Aegis (an Essar company) as a Non-Executive Director.